Everyone is asking, “How long will this market cycle last?” While predicting the exact moment is impossible, one thing is for sure—you must be ready for when the next crash comes. Unlike fictional scenarios like a zombie apocalypse, a market downturn is an absolute certainty in investing. So the question isn’t if it will come, but rather, will you be positioned to protect and grow your wealth when it does?

We all remember the financial crisis of 2008—the global meltdown that crushed portfolios and futures. But here’s a powerful truth: Not everyone lost half their savings that year. Imagine having a portfolio that declined less than 4%, while markets plummeted 50%? What if there’s a way you can build resilience into your investments, limit losses, and still pursue stock market–style gains?

Enter a strategy pioneered by one of the most influential investors of our time—Ray Dalio.

Ray Dalio and the All Weather Portfolio: Investing for Every Season

Ray Dalio isn’t a household name for most, but he’s the mastermind behind Bridgewater Associates—the world’s largest hedge fund with nearly $160 billion in assets. His insights are closely watched by central bankers, governments, and financial leaders worldwide. Driven by a vision to build a lasting legacy, Dalio created the All Weather portfolio—a game-changing investment strategy rigorously back-tested through nearly a century of market cycles.

Dalio’s genius isn’t about chasing high returns with reckless bets; it’s about minimizing losses. Conventional balanced portfolios try to smooth volatility, but during crises, they’ve plunged 25% to 40%. That’s because stocks are inherently volatile and dominate the risk exposure in such portfolios. Dalio’s approach carefully balances risk across multiple economic environments—something he calls “All Weather” because it prepares your investments for whatever season comes next.

Proven strategies for true financial freedom—no matter where you’re starting from.

What’s the biggest thing successful people have in common? They are obsessed with not losing money. How do they do it? One big way is by investing smart. They don’t necessarily take big risks. They learn from their mistakes and avoid making stock investing mistakes and other common errors. Investing mistake 1: Wrong asset allocation […]

Money: There’s nothing quite like it. Money has the power to create or destroy. It can be a blessing that turns your dreams into reality or a burden you always carry. One thing is for sure: you must become a money master, or it will master you. As Tony Robbins says, “When you lack confidence […]

Usually when we hear stories of the behavior of the super-rich it involves shopping sprees, trips to Monaco or perhaps the occasional lifestyle productivity hack. But how did the American ultra-wealthy become the top 0.01%? Is there a secret formula to obtaining and maintaining wealth? What do all rich people have in common? For four […]

Ready for a truth most people won’t tell you? No matter the state of the economy, current politics or world events, you control the amount of money you make. Current job not creating enough income? It’s time to get serious about passive income. Tony says, “If you want to change your life you have to […]

Much like stepping on the scale after the holidays, the amount of money you’ll need to comfortably retire is the number many Americans aren’t sure they want to know. In fact, half of Americans haven’t even tried to calculate how much money they’ll need to retire. However, just like those extra pounds, ignoring the problem […]

Is your workforce passionate? According to a Deloitte study, the answer is likely, “no”: 64 percent of all workers report being neither passionate nor engaged at work – including 50 percent of executives and senior management. That’s a staggering number, especially when you consider the many benefits of a passionate workplace culture. Modern workers want […]

Read Tony's Book

Of course, anybody can show you a portfolio (in hindsight) where you could have taken gigantic risks and received big rewards. And if you didn’t fold like a paper bag when the portfolio was down 50% or 60%, you would have ended up with big returns. This advice is good marketing, but it’s not reality for most people. Dalio’s greatest genius lies in his obsession with not losing money – which leads to the ultimate balanced portfolio.

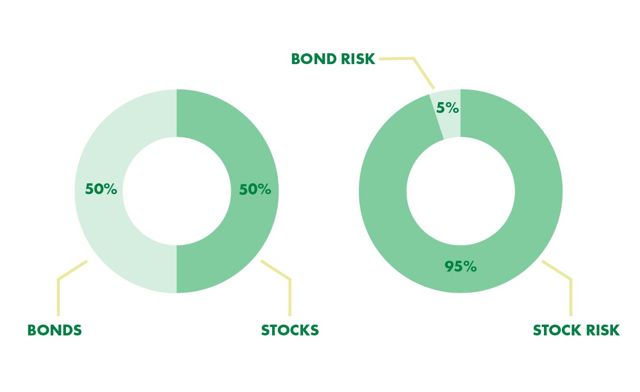

Conventionally balanced portfolios are divided up between 50% stocks and 50% bonds (or perhaps 60/40, or even 70/30 if you’re really aggressive). Conventional wisdom tells us that this balances out risk by limiting our exposure to the market. But then why did most “balanced portfolios” drop between 25% and 40% when the bottom fell out of the market? Dalio says its because stocks are three times more volatile (read: risky) than bonds. So if your stocks tank, the whole portfolio tanks.

Dalio sat down with Tony Robbins when he was doing comprehensive research for his personal finance book, MONEY: MASTER THE GAME. During their three-hour conversation, Dalio said, “When you look at most portfolios, they have a very strong bias to do well in good times and bad in bad times.”

Much like King Solomon (and The Byrds), Dalio believes there is a season for everything. He told Robbins, “Tony, when looking back through history, there is one thing we can see with absolute certainty: every investment has an ideal environment in which it flourishes. In other words, there’s a season for everything.”

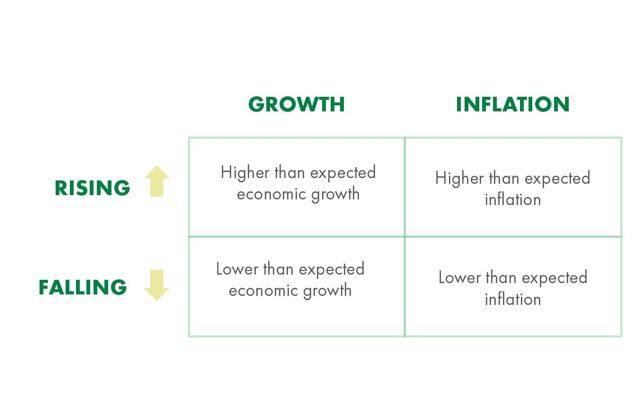

According to Dalio, there are only four things that move the price of assets:

And, there are only four different possible environments, or economic seasons, that will ultimately affect whether investments (asset prices) go up or down. (Unlike nature, however, there is not a predetermined order in which the seasons will arrive.)

These seasons are:

1. Higher than expected inflation (rising prices) 2. Lower than expected inflation (or deflation) 3. Higher than expected economic growth 4. Lower than expected economic growth

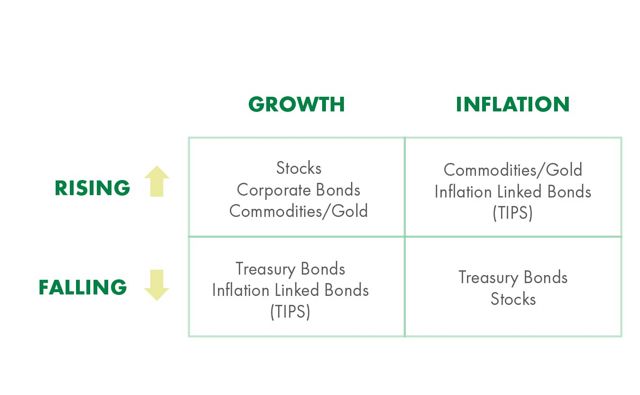

Because there are only four potential economic environments or seasons, Dalio says you should have 25% of your risk in each of these four categories – not 25% of your wealth in each category. That’s why he calls this approach All Weather: because there are four possible seasons in the financial world, and nobody really knows which season will come next. With this approach, each season, each quadrant, is covered all the time, so you’re always protected.

This chart breaks down which type of investment will perform well in each of these environments.

While it is invaluable to understand the principles behind Ray’s asset allocation, the challenge for investors is how to take these principles and translated them into an actual portfolio. Therefore, Robbins convinced Dalio to share a simplified version of his All Weather strategy. A strategy that the average person can execute, without any leverage, to get the best returns with the least amount of risk. It’s called the All Seasons strategy.

Why would Dalio give away the secret to his “secret sauce”? The last time Dalio would take you on as an investor you had to have $5 billion in investable assets and your initial investment needed to be a minimum of $100 million – but here he is, generously willing to help out the average investor.

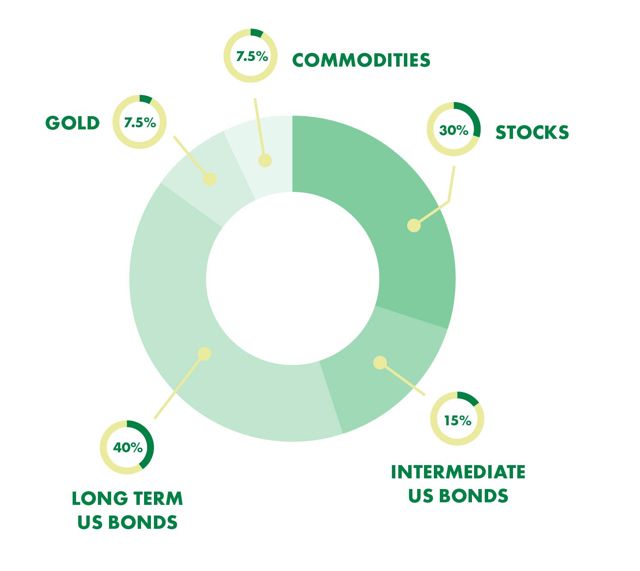

Behold the All Seasons strategy:

First, Dalio says, we need 30% in stocks — for instance, the S&P 500 or other indexes, for further diversification in this basket.

Then, you need long-term government bonds. Dalio recommends 15% in immediate term (seven- to ten-year Treasuries) and 40% in long-term bonds (20- to 25-year Treasuries). This counters the volatility of the stocks.

Finally, Dalio rounded out the portfolio with 7.5% in gold and 7.5% in commodities. As he notes, “You need to have a piece of that portfolio that will do well with accelerated inflation, so you would want a percentage in gold and commodities. These have high volatility. Because there are environments where rapid inflation can hurt both stocks and bonds.”

Lastly, don’t forget to rebalance. Meaning, when one segment does well, you must sell a portion and reallocate back to the original allocation. This should be done at least annually, and – if done properly – it can actually increase the tax efficiency. For more information on rebalancing see our article on investment strategy.

Now you’re ready for whatever comes your way, be it the longest bull run in U.S. history… or a sudden crash.

Take control of your financial future at Tony's Wealth Mastery event

Build Your Financial Fortress with the Right Strategy

Uncertainty is the one constant in financial markets. But with knowledge, discipline, and the right strategy, you don’t have to be at the mercy of the next crash. Ray Dalio’s All Weather portfolio and its simplified cousin, the All Seasons strategy, offer everyday investors a roadmap to weather any storm.

Building a thoughtfully diversified portfolio—across stocks, bonds, gold, and commodities—with regular rebalancing is your best defense and opportunity for sustainable growth. You don’t have to predict the future—you just have to prepare for it.

Take control today. Position yourself not just to survive market downturns, but to thrive through them. Your financial freedom depends on it.

Speculating on the Bull Market’s End: What You Need to Know

Look, everyone wants to know when the bull market will end. It’s the million-dollar question that keeps investors awake at night. The truth? No one — not Wall Street, not governments, not even the smartest investors — can predict the exact timing. Markets are complex living systems, influenced by countless factors that shift constantly.

But here’s what I know from decades of studying market cycles and human behavior: The bull market will end. That’s a certainty. It always does. No rally lasts forever. What separates winners from losers is not guessing the exact top, but being prepared for the downturn and having a strategy that protects your capital while positioning you for the next opportunity.

Your focus can’t be on fear or guesswork. It must be on control — controlling how you respond, how you manage your emotions, and how you position yourself financially. If you build your portfolio with resilience, hedge your risks wisely, and keep learning and adapting, you won’t need to fear the market’s inevitable corrections.

So, instead of wasting energy trying to time the market, invest that energy in mastering your mindset and crafting a winning strategy. The bull market is still here, and your job is to make the most of it while preparing to thrive when the tides change.

Disclaimer

This document is for information and illustrative purposes only and does not purport to show actual results. It is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate its ability to invest for a long term especially during periods of a market downturn. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those discussed, if any.

Legal Disclosure: Tony Robbins is the Chief of Investor Psychology at Creative Planning, Inc., an SEC Registered Investment Advisor (RIA) with wealth managers serving all 50 states. Mr. Robbins receives compensation for serving in this capacity based on increased business derived by Creative Planning from his services.