Dominate the competition

Get instant accessHave you ever thought about who chooses the funds in your 401(k) plan, and how they selected those particular funds? Why are you offered different funds than your spouse or your friend? Are they chosen based on your eligibility, or your age?

The truth is that the funds offered in your 401(k) are selected based on the investment firm’s willingness to kick back some of the fees they make off of you. In short, the funds offered are chosen based on how they benefit the 401(k) provider, not you.

So how much does the limited selection of funds really affect you? Aren’t all funds basically the same? That would be a resounding “NO.” Funds vary greatly in both their return and the fees that they charge, so the selection of funds could make the difference between a comfortable retirement and running out of money when you need it most.

This conflicted advice is costing Americans $17 billion dollars a year, according to a report earlier this year from the White House Council of Economic Advisors. You know now how 1% in fees can cost you 10 years of retirement income, so how do you select funds that will return the maximum performance at the lowest cost?

Warren Buffett gave us all the answer in a letter to his shareholders:

“Most investors, both institutional and individual, will find that the best way to own common stocks (shares) is through an index fund that charges minimal fees. Those following this path are sure to beat the net results (after the fees and expenses) of the great majority of investment professionals.”

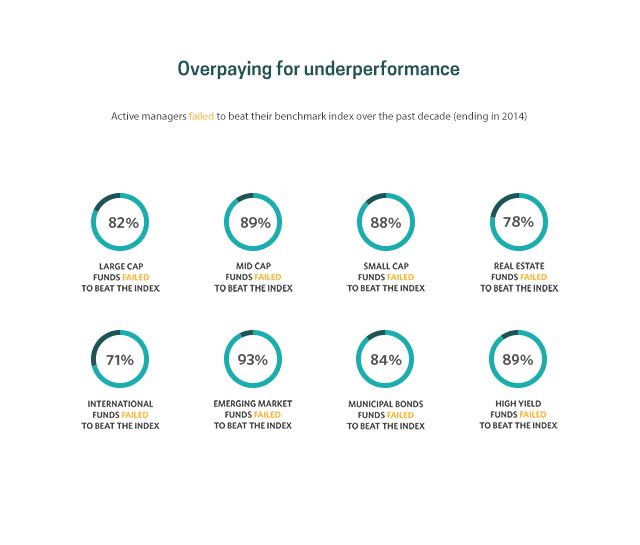

Essentially, the answer is indexing. Owning all the stocks in an index through a low-cost index fund is called indexing, or passive investing. This style is contrary to active investing, in which you pay significantly more in fees (sometimes 10 to 30 times more!) to a mutual fund manager to make choices about which stocks to buy or sell. The active manager wants to beat the market, but study after study shows that few actually do.