There isn’t a single portfolio manager, broker, or financial advisor who can control the primary factor that will determine if our money will last. It’s the financial world’s dirty little secret that very few Americans know. And of those who do, very few will ever dare bring it up. That’s why I went to my dear friend, the late Jack Bogle.

Jack Bogle was the founder of the world’s largest mutual fund, Vanguard, and about as straightforward as a man could be. When we spoke for four hours in his Pennsylvania office, I brought up the dirty little secret, and he certainly didn’t sugarcoat his opinion or thoughts.

“Some things don’t make me happy to say, but there is a lottery aspect to all of this: when you were born, when you retire, and when your children go to college. And you have no control over that.”

What lottery was he talking about? It’s the big luck of the draw: What will the market be doing when you retire? If someone retired in the mid-1990s, he was a “happy camper.” If he retired in the mid-2000s, he was a “homeless camper.”

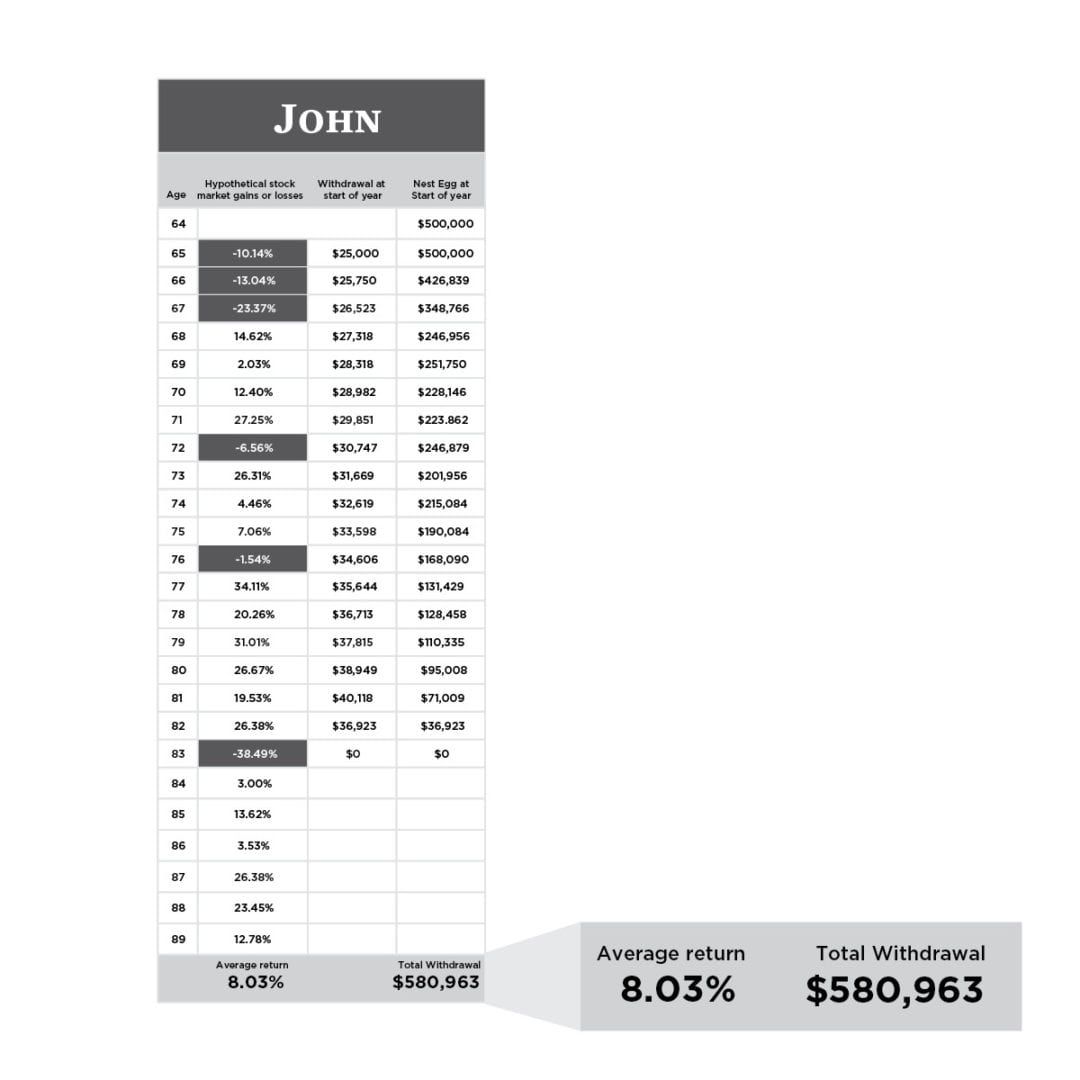

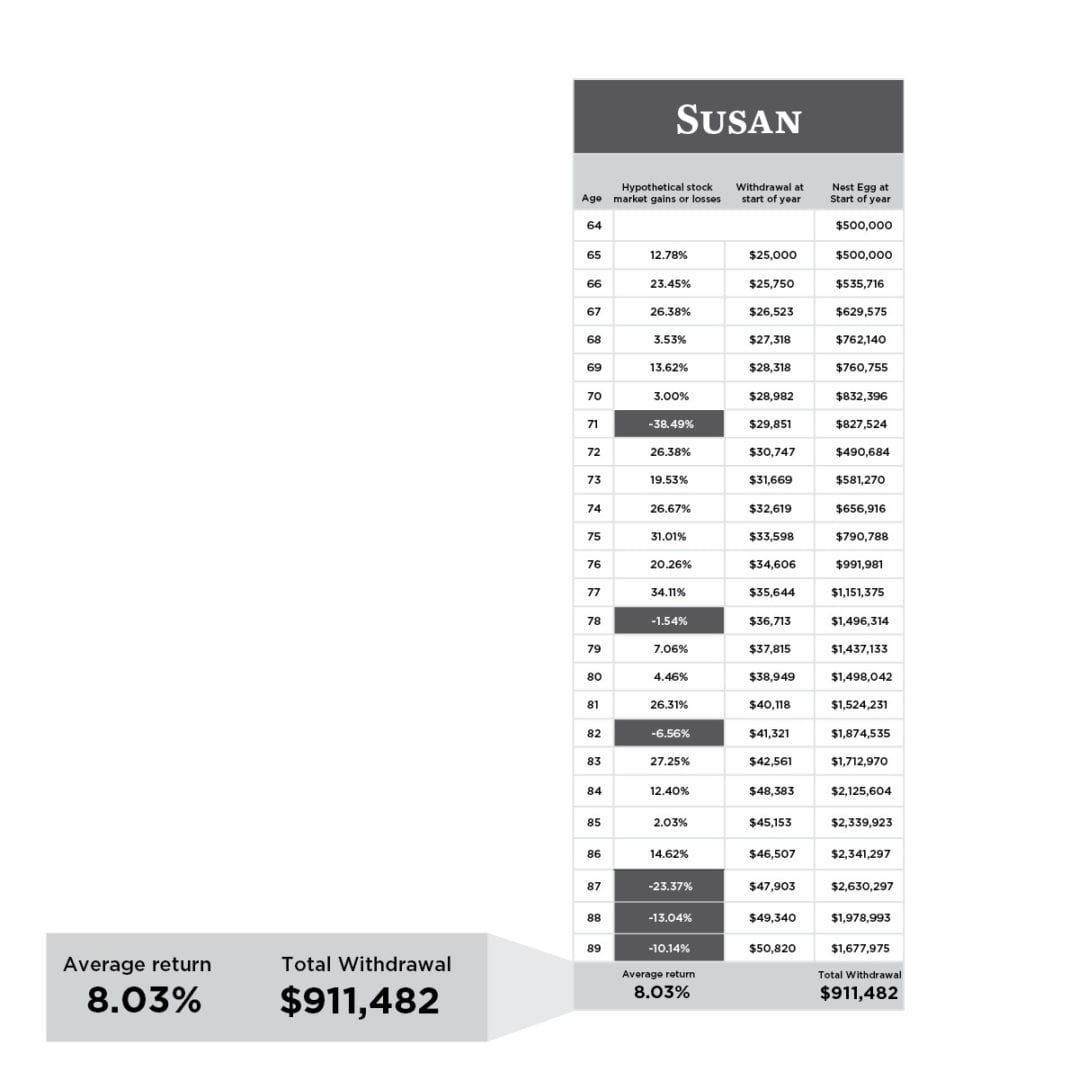

Understand the sequence of returns

The risk we all face is the devastating concept of sequence of returns. Sounds complicated, but it’s not. In essence, the earliest years of your retirement will define your later years. If you suffer investment losses in your early years of retirement, which is entirely a matter of luck, your odds of making it the distance have fallen off the cliff.

You can do everything right: find a fiduciary advisor, reduce your fees, invest tax efficiently, and build up a Freedom Fund. But when it’s time to ski down the backside of the mountain, when it’s time for you to take income from your portfolio, if you have one bad year early on, your retirement plan could easily go into a tailspin. A few bad years, and you will find yourself back at work and selling that vacation home.

Sound overly dramatic? Take a look at John and Susan.

John is now 65 and has accumulated $500,000 (far more than the average American) and is ready to retire. Like most Americans nearing retirement, he is in a “balanced” portfolio (60% stocks, 40% bonds). Since interest rates are so low, John decides he will need to take out 5%, or $25,000, of his nest egg each year to make his income needs for his most basic standard of living. When added to his Social Security payments, he “should” be just fine. And he must also increase his withdrawal each year (by 3%) to adjust for inflation because each year the same amount of money will buy fewer goods and services.